")

Pixel Fit/E+ (via Getty Images)

Bain Capital Specialty Finance (New York Stock Exchange:BCSF) started out of curiosity for me. I recognized Bain's name because it had gained notoriety since the 2012 presidential election, when it negatively affected the Romney campaign.I found it naturally I'm tempted to take a look at this company and see what's out there.

Overall, we found this to be a decent business with a safe risk profile and an attractive yield of just over 11%. It may not be the best deal ever, but at current prices it's a “buy”.

Relationship with Bain Capital

What is your relationship with Bain Capital? Our most recent Form 10-K (page 6) clearly states:

Bain Capital Credit is a wholly owned subsidiary of Bain Capital, LP (“Bain Capital”) and the Advisor is a majority owned subsidiary of Bain Capital Credit.

There are several layers here, but essentially BCSF is a fund that allows Bain Capital to earn additional income through management fees.

investment approach

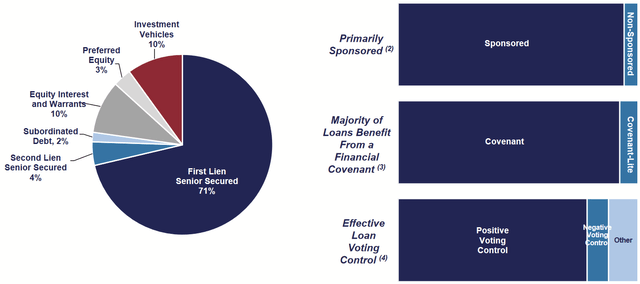

Like many of its peers, the fund trades with private companies and offers these opportunities to shareholders through BCSF's public stock. The firm invests primarily in the middle market, defined as companies with annual EBITDA in the range of $10 million to $150 million.

Q3 2023 Company Presentation

The company's preferred investment form is secured first or second lien loans. To a lesser extent, they opportunistically issue junior debt, invest in stocks, and purchase other investments. Almost all of these loans have variable interest rates.

Leveraging Bain Capital Credit's resources and contacts, BCSF derives investment ideas, performs due diligence processes, seeks credit committee approvals, and closely monitors portfolio company performance (2022 Form 10-K, pg. 8). Due diligence often involves interviews with management and on-site visits to obtain a stronger practical understanding of business fundamentals.

First and foremost, BCSF's investment priority is to minimize risk.

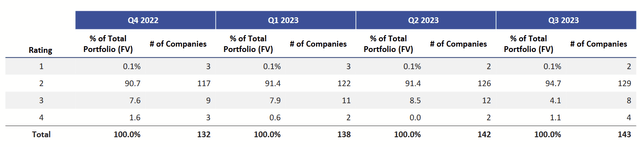

Many of our investments have credit ratings that are considered below investment grade. As a result, it has created a 1-4 rating scheme to give the company its unique view of its portfolio (page 11).

- Investments that outperform expectations.

- One that performs as expected.

- One that performs lower than expected.

- Those with significantly degraded performance.

Q3 2023 Company Presentation

As of Q3 2023, nearly 95% of the portfolio was in Tier 1 or Tier 2.

Q3 2023 Company Presentation

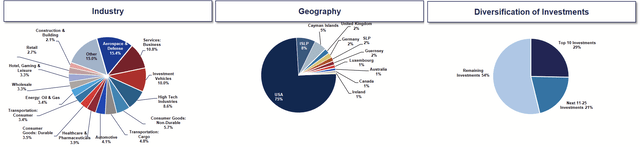

Although this fund is primarily diversified, there are some subtleties as well. In the slide above (cropped for convenience), BCSF's 122 portfolio companies are in dozens of industries, primarily in the United States. The top 10 investments account for approximately 29% of the portfolio.

financial history

This company's financial history is not as extensive as other companies. Bain Capital has been around for a long time, but BCSF he made his IPO in 2018. As a registered investment company, it must distribute most of its profits as dividends, so let's take a look at its history.

Dividends and capital

In search of alpha

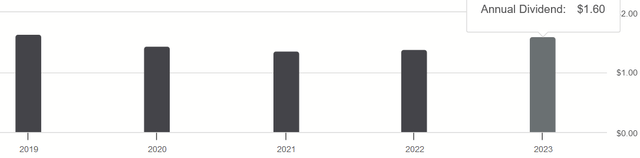

Over the past five years, the company has paid annual dividends per share (on a quarterly basis) ranging from a low of $1.36 to a high of $1.64. What factors influenced this? First, the various challenges in the macro environment caused by COVID-19 clearly had an impact.

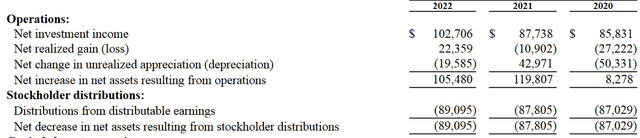

Changes in net assets (2022 Form 10K)

Secondly, I think it's important to recognize how this business is capitalized.

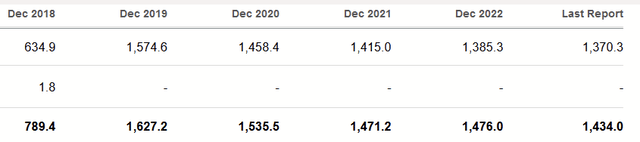

Number of shares outstanding (we are looking for alpha)

Fundraising continued after the IPO, but since 2020, the number of outstanding shares has remained at 64.6 million.

Long-term debt (in search of alpha)

Similarly, the company has been repaying long-term debt since 2019. Due to distribution requirements, it is common for many BDCs and similar companies to periodically sell stock to raise more capital. Many investors automatically reinvest their dividends, effectively allowing these companies to keep their profits for investment and pursue growth opportunities.

BCSF doesn't do anything like that here, but I think that's interesting. It works on the same balance sheet and carries forward any unused expenses, losses, and distributions. So why is the dividend going up? During the third quarter 2023 earnings call, Michael Boyle (President) explained:

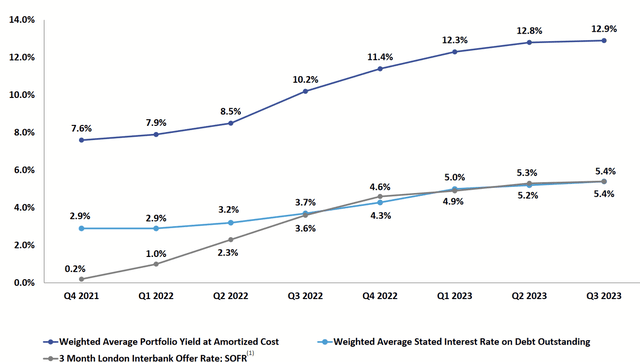

As of September 30, 2023, the weighted average yield of the investment portfolio at amortized cost and fair value was 12.9% and 13.1%, respectively, compared to 12.8% and 13% as of June 30, 2023. did. This increase is primarily due to the following factors: By increasing the reference interest rate on our loans. In addition, 94% of our fixed income investments earn interest at a variable rate.

As interest rates have risen, so have the dividend yields for shareholders.

Portfolio Yield Spread (Q3 2023 Corporate Presentation)

risk profile

Q3 2023 Company Presentation

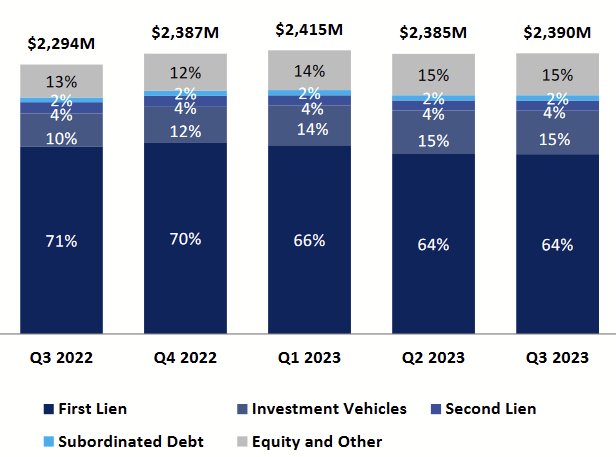

Others have noticed a continued decline in their portfolio's concentration in first-lien debt. However, this is based on how companies report their assets. As revealed in the same financial report:

As we emphasized to shareholders in our previous earnings call, the reduction in our initial lien exposure is due to the growth of our joint ventures. Specifically, 94% of the underlying assets held in these investment vehicles consist of first-lien loans, resulting in approximately 82% of the portfolio having first-lien exposure.

As such, the company has maintained its commitment to the collateral provided by first-lien debt.

Outlook for the future

Concerns about the strength of U.S. regional banks remain as the fourth quarter of 2023 results approach. This could be fertile ground for BDCs such as BCSF. In the aftermath of the 2008 financial crisis, major banks reduced their exposure to the middle market in favor of large corporations. A similar possibility exists if local banks find themselves in a bind due to a commercial real estate bubble. Once capital is depleted, a well-prepared BDC can attract a wider pool of candidates and command higher yields with tighter covenants, allowing them to earn higher returns with lower risk.

Additionally, while the law only requires an asset coverage ratio of at least 150%, BCSF recently reached 182.2% (Form 10-Q, page 131). This gives you more room to leverage for growth among better investment options. I think this will be important to monitor as Q4 results are released and U.S. commercial real estate loans are tested throughout the year.

That aside, we also need to consider the future of dividends, as they are the main way shareholders receive profits. Since the actual stocks are only a small portion of the portfolio and most of the dividend growth comes from the benefit of a floating rate portfolio, a reversal in interest rates could just as easily reduce the distributable income. Rate hikes have been paused, but it remains to be seen how long it will be before a rate cut is announced.

evaluation

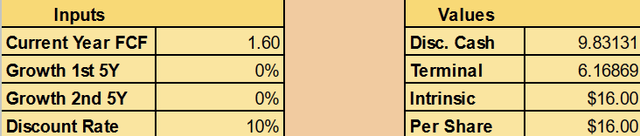

Since the draw is a dividend, we evaluate this using discounted cash flows. We will use the 2023 total distribution of $1.60 per share as our baseline. We do not assume any growth as we recognize that there is a mix of potential for revenue increases and decreases. Since BDC yields are also often in the 10% range, we use a terminal multiple of 10.

Author's calculations

it is $16 intrinsic value flat.

conclusion

Bain Capital Specialty Finance has been a consistently profitable business since its inception, offering high (if volatile) dividend yields even in challenging environments. I think yield-loving shareholders are relatively well off because their portfolio is invested in collateralized debt and management is in no rush to grow the balance sheet with continued financing. If interest rates remain high while the local banking industry's woes materialize, BCSF may be well-positioned to ride the wave.

No matter what happens, I think this stock is a reasonable buy at a modest discount to non-growth stocks.